17.07.2026

Cut to the Bone: Farmers at the mercy of the meat monopolists

How state authorities put France’s farmers at the mercy of an industrial giant

Published with

INVESTIGATION

The spectre of industrial scale farming looms large in the French consciousness. Mixed family farms make way for ever larger operations with mono-culture crops or industrially farmed animals.

Farming groups blame years of low prices, which helped fuel the farming protests that erupted in 2024. France’s opposition to a Brussels-led trade deal, which threatens to open the doors to cheap Brazilian beef, has become a divisive political issue.

But the march towards industrial scale meat production may have been set in motion over a decade ago through domestic decisions over how the French government protects, or fails to protect, sustainable practices along the beef supply chain.

France, Europe’s largest beef producer, underwent a quiet restructuring in the late-2000s. A wave of mergers, green-lit by state authorities, concentrated the sector in the hands of a single large group which now dominates national slaughtering capacity.

At the centre of this consolidation stands Groupe Bigard, a family-controlled company that, through successive acquisitions in that period, came to handle roughly one in every three cattle slaughtered in France.

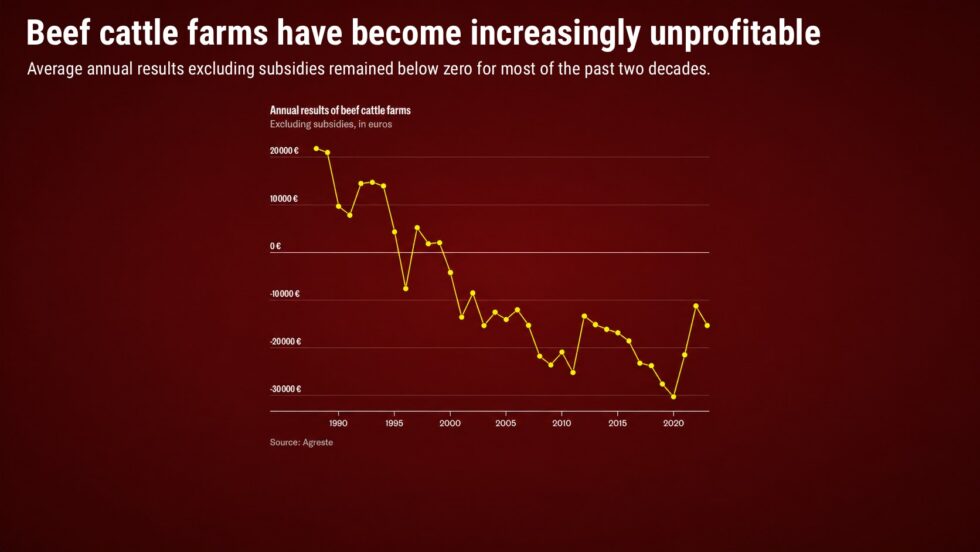

Since this radical restructuring, France has lost a quarter of its cattle farms. For much of the next decade prices paid to farmers stagnated and pre-subsidy losses increased by 50%. By 2020 the average cattle farm made annual losses of €30,000.

Public subsidies increasingly bridged the gap between farmgate prices and production costs. A state audit in 2022 found that processors are absorbing taxpayer money meant for cattle farmers by exploiting farmers’ lack of bargaining power.

As prices stagnated, meat processors captured a growing share of every euro that consumers spent on supermarket beef. Over the period during which farmgate prices fell, Bigard’s profitability grew: Bigard increased its margins, earned record profits and collected hundreds of millions of euros in dividends.

For some farmers, the years of losses meant a stark choice: go big or get out. For some, this has meant converting to cereal farming, where they can earn a healthier income – and have the freedom to take a weekend or holiday. For others, it meant the loss of their livelihoods – and their way of life.

This investigation has endeavoured to understand how a handful of big French slaughterhouse firms, led by Bigard, ended up with so much power, which farms across France are most impacted and whether the concentration of market control is legal. To do this we needed to establish:

This methodology explains how we sought to establish the actual markets that farmers sold into and their structure, to put farmers first, rebuilding the market from their perspective. We assessed whether the championing of “consumer welfare” was in fact benefitting consumers – or corporations.

Once we figured out how farms and slaughterhouses were distributed and who owned the slaughterhouses they could reasonably drive to, we could use established indices for measuring market concentration under distance assumptions that reflect actual transport limits to figure out where farmers were very likely being squeezed.

Our objective was straightforward: to replace an abstract, national view with a farm-level picture of buyer power, showing where choice has thinned to a vanishing point and how regulatory framing enabled the quiet consolidation of Europe’s biggest beef market.

Finally, after establishing market concentration, we take a closer look at the winners and losers by quantifying the gains and losses of farmers, slaughterhouses, taxpayers and consumers.

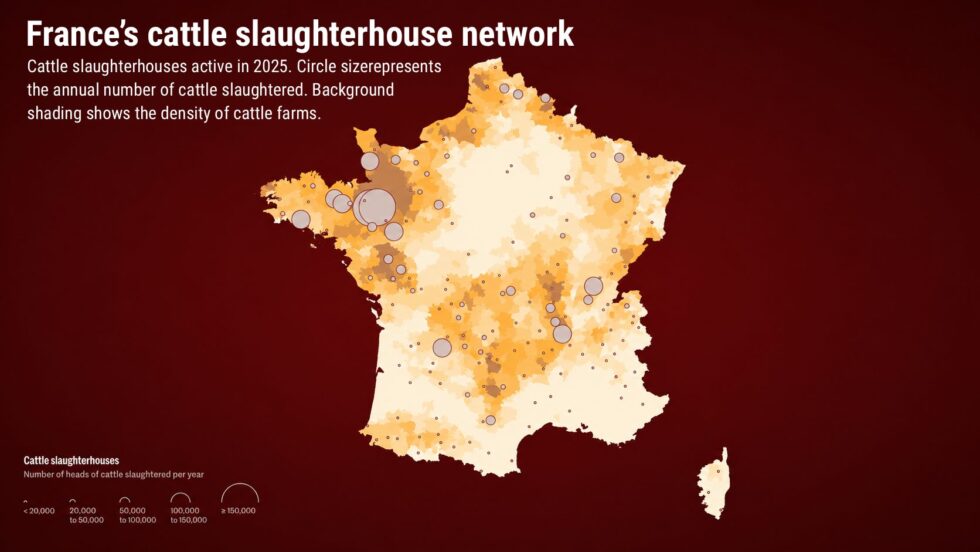

In order to understand the meat processing industry in France, the first step was to build a comprehensive dataset of cattle slaughterhouses in mainland France, including where they are located, who owns them and how many cattle they slaughter annually. This data was not easily accessible.

Earlier versions of this analysis relied on total site capacity from Géorisques and an Agreste map (page 4) showing species-level production bands. After further requests for information, we obtained more precise data from the statistical service of the French Ministry of Agriculture. The ministry’s response was based on two administrative sources, the monthly survey of large-animal abattoirs (slaughterhouses) (DIFFAGA) for abattoir production, and the national cattle identification database (BDNI) for cattle movements between farms and abattoirs.

The ministry provided a file of cattle abattoirs active in 2025. For each abattoir, the file gave the commune code, Lambert 93 coordinates and a cattle-slaughter class, expressed as the annual number of heads slaughtered. These classes were:

Because the ministry data gives production in bands rather than exact annual figures we converted each class into a numeric estimate. For the middle classes, we used the midpoint of the band: 35,000, 75,000 and 125,000 cattle. For the open-ended top class we used the lower bound of 150,000 cattle to avoid overstating the size of the largest industrial sites. For the lowest class which includes many small local abattoirs and could range from very small annual throughput to just under 20,000 cattle, we used 2,000 cattle in our baseline scenario.

We then supplemented the ministry abattoir file with information from the European commission’s list of EU-approved slaughterhouses, Géorisques and the Institut National de la Propriété Industrielle (INPI).

The EU Register was used to identify matching establishments and SIRET numbers; Géorisques and manual corrections were used to replace commune-centre coordinates with the actual site coordinates where available and INPI and manual ownership checks were used to group sites under the companies that ultimately control them.

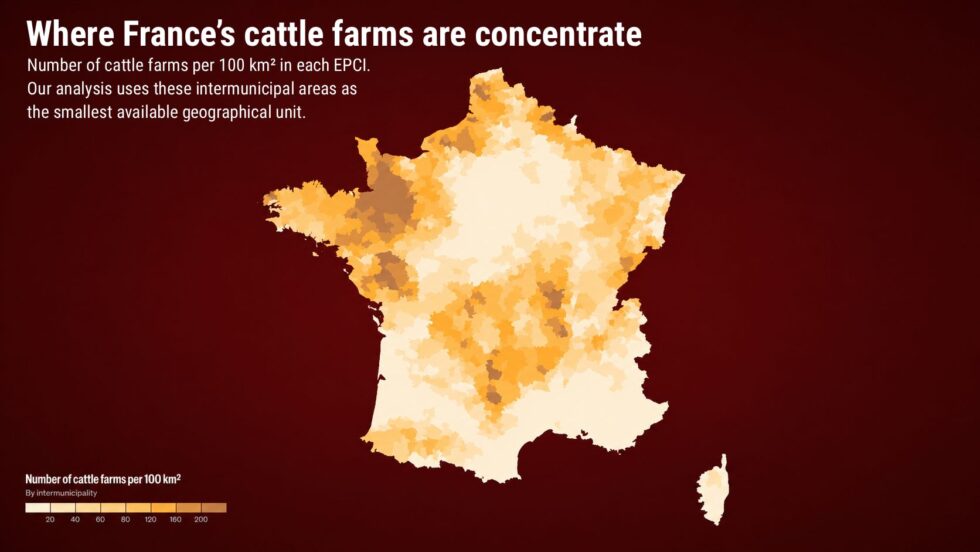

Detailed information about individual farms and their cattle is not publicly accessible in France. Instead, the ministry provided an Établissement Public de Coopération Intercommunale (EPCI) level file detailing the number of farms that sent animals to slaughter in 2025 in each EPCI. EPCIs are inter-municipal groupings of communes, they divide France into more than 1,200 local areas, giving us far more geographical granularity than departments or regions.

As such, EPCIs are used as the smallest geographic unit in our analysis. Each EPCI is represented by a centre point and the number of cattle exploitations in that EPCI is used as a weight when aggregating results.

This distinction is central to interpreting the results. When we write that a given share of “exploitations” faces a concentrated market, we mean that those exploitations are located in EPCIs whose estimated slaughterhouse market meets those conditions. We do not know the precise location of each exploitation within the EPCI, nor do we know the exact slaughterhouse used by each individual farmer.

The ministry applied statistical privacy protection where fewer than three exploitations were present, or where one exploitation represented more than 85% of the number of cattle slaughtered. These suppressed values were marked as -999. In the preprocessing step, we replaced suppressed exploitation counts with “1”, keeping the EPCI in the analysis while applying a minimal weight.

This avoids dropping EPCIs affected by statistical secrecy altogether. Since statistical secrecy only affects a small minority of EPCIs, and those EPCIs are assigned the smallest possible positive weight, this choice has limited impact on the analysis results.

Once we had the details of the slaughterhouses and EPCIs, the next challenge was to determine which slaughterhouses were realistically reachable from each EPCI. Because farmers transport live animals by road and road access affects the realistic set of slaughterhouses available to them, the core analysis uses routing distance rather than straight-line distance.

For every EPCI, we used OpenStreetMap’s Open Source Routing Machine API to calculate road distance and travel time to all slaughterhouses within 520km, based on the geographical coordinates listed in Géorisques.

We then evaluated concentration within three driving-time ranges, 1h30, 2h30 and 4h, chosen from an Agreste report as roughly the 50th, 75th and 90th percentiles of travel times for beef cattle in France. We recognise that these percentiles are conservative because they themselves are an outcome of market pressures potentially driven by consolidation

For every EPCI and every radius, we selected the slaughterhouses reachable within that travel time. We then summed the estimated annual cattle slaughter of all reachable sites and grouped those estimates by ultimate owner. This produced for each EPCI, a local buyer market, not the market from the perspective of the meat buyer, but the set of slaughtering options realistically available to cattle farmers in that area.

There are no international standards that define an unfair level of market concentration for slaughterhouses so we tested several different approaches. In addition to looking at the standards applied by the French Competition Authority, we measured market concentration using three standard indicators: market share, the concentration ratio (CR) and the Herfindahl–Hirschman Index (HHI).

The metric used by the French Competition Authority assumes that any cattle farmer in France can sell to any slaughterhouse in France as if it were like most shelf-stable consumer goods. For example, because meat is easily storable and transportable, buyers can source meat from across the country. Hence, the relevant geographic market for meat is national.

Two of the three major Bigard mergers were assessed nationally: treating live cattle like packaged meat, storable and easy to ship. In reality, live animals are neither. Cattle lose weight (and hence value) when transported; they can also lose condition, which also affects their value.

By defining the market at a national scale, the Competition Authority’s analysis ignored what were growing pockets of high market concentration in regional markets.

The French Competition Authority is also supposed to assess mergers in relation to whether they strengthen a buyer’s power such that its suppliers become economically dependent on that buyer.

Where the Competition Authority did perform regional analyses, thresholds for economic dependence were set high enough to overshoot the point at which experts say that farmers would lose bargaining power.

Market share is a fairly straightforward approach to determining unfair competition. A farmer with three potential buyers can go to the highest bidder, forcing the lowest bidder to raise its prices, but a farmer with only one potential buyer doesn’t have this ability. Because of this, a company holding such a monopsony position has the ability to lower prices for farmers. Similarly, two buyers with no serious competitors in a region, it may be in their long term best interest to collude not to raise prices.

Market share is a simple calculation of what a single company controls in a specifically defined market. When a single company holds a 50% market share or greater, European competition law presumes that it becomes “dominant” and could impede effective competition. European courts have found dominance at market shares of 40%. Dominance is an important threshold: both French and European merger law typically treat creation or strengthening of a dominant position through a merger as unlawful.

The concentration ratio (CR) sums the market share of the leading firms. This metric focuses on the risk of a few big players dominating an industry. CR can be important in defining “collective dominance” – the risk that dominant parties will tacitly collude. The European Commission has found “collective dominance” where three companies control 79% of the market.

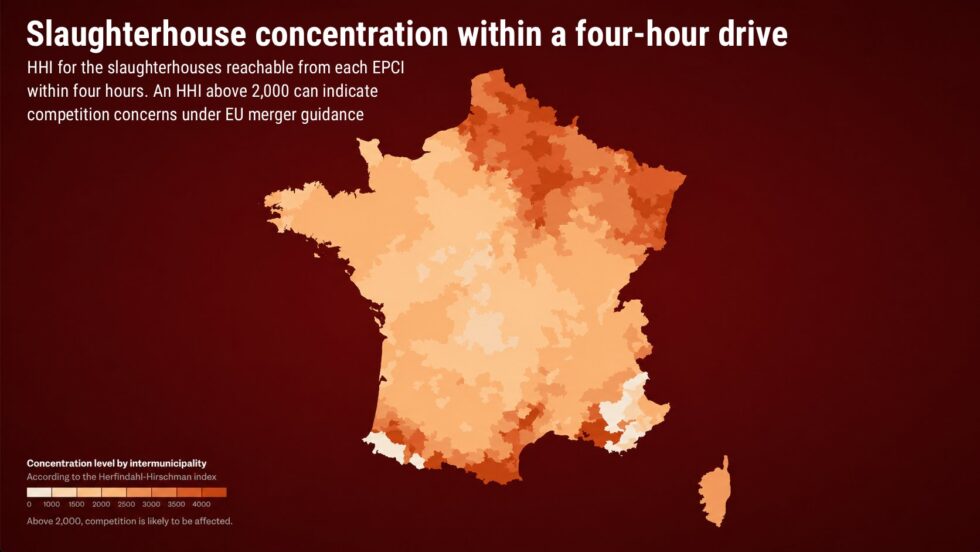

The HHI index is even more sensitive to the potential of market manipulation when a few big players in the industry are dominant. The HHI gives greater weight to more powerful firms by summing the squares of the market shares of all market participants. In EU merger guidance, an HHI above 2,000 can signal competition concerns. In the United States recent guidance is stricter with values above 1,800 deemed presumptively unlawful, meaning regulators view mergers that would exceed that threshold – along with a change of greater than 100 points – as likely to harm competition.

The US guidance states that such concentration metrics, “indicate that a merger’s effect may be to eliminate substantial competition between the merging parties and may be to increase coordination among the remaining competitors after the merger.”

For each EPCI and within each analysis radius, we calculated the number of reachable slaughterhouses and distinct buyers, computed the top two buyers’ combined market share (CR2), and measured the HHI score.

These EPCI-level estimates revealed a landscape far more concentrated than official competition analyses suggest, in which the majority of relevant markets are controlled by just one or two firms.

While national figures used by the French Competition Authority may suggest a competitive market, in the cattle producing regions of France, real choice has largely disappeared. Farm-level analysis shows that French cattle producers in several regions now sell into what are, in practice, monopolies or duopolies.

At a national level, our results show that concerning levels of concentration have become the norm for French farmers: almost two thirds of farms (64%) are in EPCIs facing markets with an HHI over 2000, which would be likely to cause competition concerns in EU law. That is the case even within the most liberal 4 hour distance threshold, within which 90% of cattle are sold. Three quarters of farms face HHI levels which would be presumptively unlawful under US merger law, at the same liberal distance threshold.

These figures are part of a structural pattern rather than a regional anomaly: EPCIs with HHI values exceeding 2000 are spread across every region of mainland France, excluding Paris.

At the local level, the majority of farms are located in EPCIs with a local duopoly operating within 1.5 hours, the distance within which 50% of cattle are transported for slaughter.

Market concentration has been driven by a wave of mergers – mostly between 2006 and 2009 – that reshaped France’s slaughterhouse network into an industrial empire.

To assess how Bigard’s acquisitions reshaped market structure, we reconstructed historical ownerships publicly available merger documentation. For each slaughterhouse, we reverted ownership to their previous parent companies and recalculated concentration metrics under both “before” and “after” scenarios. This allowed us to measure how many farms moved into highly concentrated markets once the mergers took effect.

Through successive acquisitions of Arcadie Centre Est, Charal and Socopa, Groupe Bigard acquired abattoirs which on current slaughtering volumes, increased its control of French slaughtering capacity from around 12% to 35%, consolidating what had been a fragmented market into one in which his company dominated.

Taking a longer view, between 1998 and 2020, Bigard acquired slaughterhouses which, on today’s slaughter volumes, took the company’s control from 9% to 36% of the market.

Those takeovers created or strengthened Bigard’s dominant position for EPCIs home to 63,785 farms – suggesting that 1 in 5 French farmers face markets that would generally be considered unlawful under French merger law.

Competition authorities approved some of the largest of these mergers on the assumption explained above that live cattle could be traded freely across France. Our spatial analysis, using realistic driving times, shows that within those ranges, meaningful competition has largely disappeared.

The failure of competition authorities to take account of the regional nature of cattle slaughtering is visible in the geographies of Bigard’s dominance. In several cattle producing areas, farmers now face local markets where Bigard’s market share would generally be considered unlawful under French merger law.

Mapping the results reveals those clusters of dependence in the North East and in the South West of the country.

Across northeastern France, many farms are now effectively bound to one dominant slaughterhouse within practical delivery range.

EPCIs home to 75% of farms in Grand Est now face a Bigard dominant market. The median Bigard market share in the Grand Est now stands at 61% at 2.5 hours driving distance – compared to just 19.5% before the mergers of Socopa, Arcadie and Charal.

Bigard obtained two slaughterhouses which now dominate the region through mergers in which the authorities failed to analyse the markets on a regional level – meaning that Bigard’s emerging dominance was not recognised in those decisions.

Similar dynamics have occurred in Occitanie, where three in every five farms is located in EPCIs in which Bigard is dominant.

To see how market concentration may translate into real losses for farmers, we extended our work beyond structural measures and into prices and profits across the beef supply chain.

To trace how value moves from farm to shelf, we combined farmgate and consumer price data from national sources.

Each source covers different timeframes and levels of detail. We harmonised them into comparable monthly series by aligning dates, standardising units, and where needed, we indexed series to a common base year, for instance 1995 for the CPI and national GBEA series.

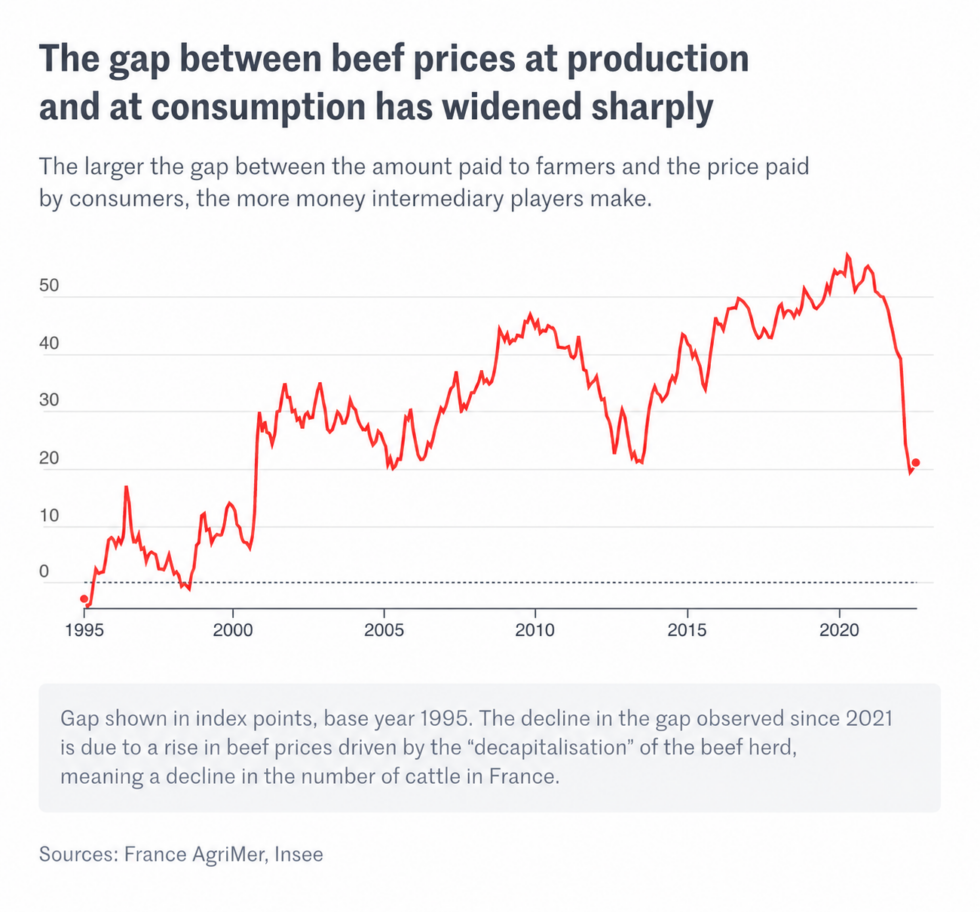

According to experts, a strong indicator of a meat processor using its market power to squeeze farmers or gauge customers is an increase in the “price spread”: the difference between the farmgate prices – what a slaughterhouse pays to farmers- and the price the slaughterhouse charges the supermarkets.

France’s Observatory of Food Prices and Margins has published annual reports which provided a composite of price spreads since 2013. These reports show that between 2013 – 2019, the processors’ share consumer prices increased by 18.5% while farmers’ share fell by around 11%.

We wanted to compare spread data from before and after Bigard’s major mergers.

As the Price Observatory data is not available for the-pre merger period, we analysed data on farmgate prices and consumer beef price indices obtained from the statistical institute, INSEE.

This analysis showed that between the pre-merger period and post-merger period, the spread nearly doubled, from 25 to 48 points. This arose from an underlying trend between 2013 and 2021 during which farmgate prices fell by more than 10%, while consumer prices rose by around 10%.

This trend reversed from 2021: in recent years those trends have reversed as constriction in supply has led to steeply increasing prices for cattle. These price increases pushed spreads back to pre-merger levels. This reversal suggests that the inflationary shock after 2021 was partly absorbed at the buyer level, with limited transmission to consumer prices.

To link these price dynamics with company-level profit margins, we turned to company accounts from Pappers covering the leading operators in France’s red-meat sector from 2013 onwards; and an analysis of Bigard’s financial statements for the pre and post merger period.

The dataset includes annual revenues, cost of sales and net incomes, for major groups such as Bigard, Elivia and Sicarev. This allowed us to show how Bigard’s companies achieved increased profitability in the years following consolidation, and how they compared to competitors.

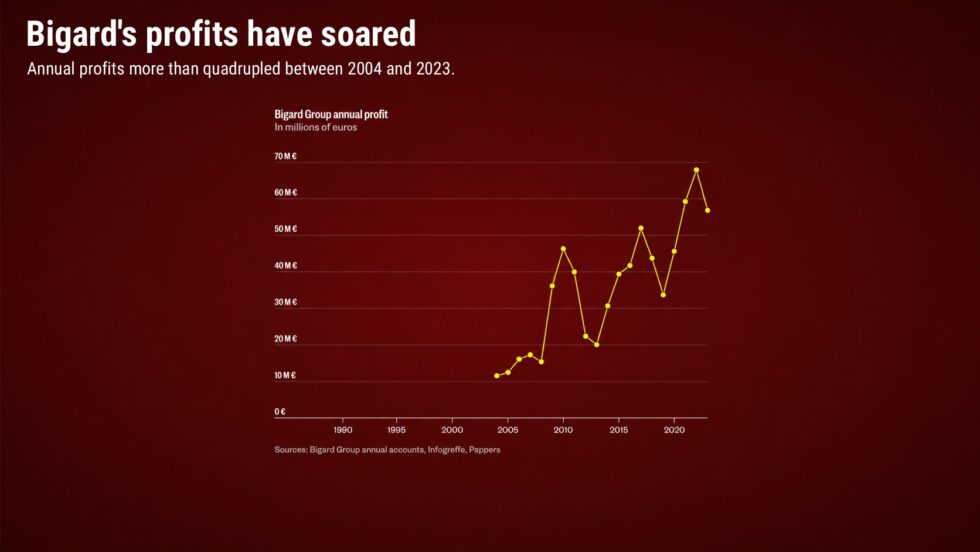

Groupe Bigard has paid €300 million dividends over the last decade.

Since the 2006-2009 merger wave Groupe Bigard, the main operating company of the group, increased its operating profits more than fourfold. Its operating margins more than doubled between 2004 and 2022.

Between 2013 and 2020, during which our price series shows that “price spread” was drastically increasing, Bigard’s main operating companies increased their gross profit margins from 27% to 32%, reinforcing the notion that farmers were getting a smaller share of every unit of revenue earned by Bigard.

Bigard is significantly more profitable than most of its competitors. Amongst the top red meat processors in France, Bigard controls around 45% of revenues, but 61% of the profits. The company commands significantly higher profit margins than all competitors in red meat except Cooperl, which has the second largest share in the pork market. Its average profit margins are more than three times those of its closest competitor in the beef processing industry.

Numerous academic experts who have reviewed our methodology and results have told us that they raise important questions which the Competition Authority should consider.

We would like to thank Professor Peter Carstensen, Austin Frerick, Claire Lavin, Dr Martin Csirszki, and Aurélie Catallo for reviewing our methodology and for their helpful comments and questions.

All datasets used in this investigation have blind spots. We have made these limits explicit so readers can see where our analysis is strong and where uncertainty remains.

Each stage of the analysis, from data collection to concentration metrics, can be retraced through intermediate files and scripts, allowing others to verify or build on our results.

France keeps current registers of approved slaughterhouses, but neither the European Commission’s EU Register nor national databases like Géorisques preserve complete historical entries. As a result, it is not possible to reconstruct precisely when all abattoirs closed, when they changed ownership, or when their capacity changed over time.

The Ministry of Agriculture data improved our current picture of the cattle slaughtering market by providing 2025 cattle-specific production bands for abattoirs. However, this data is also available for only one point in time. It does not show how each site’s cattle slaughter volumes evolved before, during or after the merger waves analysed in this investigation.

Because of these gaps, we can describe the structure of today’s market and retrace how part of that structure was formed, but we cannot model how local concentration evolved year by year.

For that reason, our “before and after” estimates rely on reverting the ownership of current slaughterhouses to their previous parent companies, using publicly available merger documentation. This reconstruction captures the effect of ownership consolidation among sites that are still operating today, but it cannot reflect abattoir closures, or capacity changes that occurred since those mergers.

An ideal price analysis would look at how the spread between farmgate, slaughterhouses and supermarket prices changed over time. France’s Price Observatory mentioned in the “Comparing farmgate and consumer trends” publishes annual reports including some of this data. However these were of limited use for comparing longer time periods: most annual reports only provide a 5 year window (starting in 2012). Because the Observatory’s figures are derived from a formula which changes each year and is not available to us, we were unable to combine figures from different reports to measure spreads for the entire period.

Similarly, the GBEA price series offers regional figures only from 2013 onwards and only for four large areas, compared with Metropolitan France’s usual 13 regions. This prevents us from tracking how prices evolved from before the main mergers (2006–2009) to today.

The lack of a more regional breakdown also means that short-term shocks, such as disease outbreaks or export bans, cannot be fully disentangled from concentration effects. Such shocks are what could allow us to test how sensitive prices are to market changes.

Our ownership and capacity data show how the slaughtering market is structured, but they don’t reveal the private contracts or supply agreements that can shape farmers’ real options. In some cases, as Bigard told parliament, processors help fund producer groups. These ties are not transparent, and the details are not made public and therefore can’t be factored into our analysis.

We measured price-transmission elasticity – the ratio between consumer price movements and farmgate price movements over time. From 2004-2006, before the main mergers of the late-2000s, transmission between farmgate and retail beef prices was weak but mostly aligned: the median elasticity was 0.12, and retail prices moved opposite to farm prices in about 40% of months.

After consolidation (2017-2019), the relationship shifted in direction. The median elasticity turned slightly negative (-0.06) and the share of months with inverse movements rose to 57%. Whilst these figures are consistent with weaker transmission from farmgate to retail prices after consolidation, the sample periods were too short and the relationship too noisy for these figures to be conclusive.

We also looked at whether Bigard’s operating companies showed a clear pre- and post-merger shift in gross profits, but the results were inconclusive.

We were able to do some comparisons to other major beef producing countries but the results of this analysis were inconclusive. The European Union publishes data on carcass prices across all member states, starting in 2002, and live cattle prices starting in 2014. We compared France’s prices to the European average as well as Germany and Italy, the next largest producers.

French carcass prices are around the same as Germany, and generally lower than Italy. Whilst Germany has a less concentrated market than France, reliable market share data was not available from Italy.

Until 2014 carcass prices in France closely tracked EU average prices. Since 2014, French carcass prices have fallen below the weighted average price across the EU. This is mirrored in the price of young male cattle, in which France has trailed the EU average for much of the last decade.